Written by Jon Scheele, organiser of APIdays Singapore and co-organiser of API Craft Singapore

To thrive in the digital economy requires linking activities across industry specialisations. The insurance distributor-producer-reinsurer model has broadened to include many more players, while customers expect a seamless experience. Open Insurance provides an approach for managing the complexity and a foundation for innovative new business models.

Marketplace platforms help buyers and sellers find and transact with each other. Platforms in business-to-consumer (B2C) markets are well established, including e-commerce (Amazon and eBay in the USA, Alibaba, Lazada Rakuten and Bukalapak in Asia), ride-sharing (Uber and Lyft in the USA, Grab and Go-Jek in South East Asia), and travel (Trivago, Skyscanner, Wego, Tokopedia, etc.). Platforms are also pervading business-to-business-to-consumer (B2B2C) and business-to-business (B2B) markets.

In this platform world, insurers have a choice:

- Become a platform: Orchestrating the combination of products and services to meet your customers’ holistic needs, or

- Make yourself pluggable: Make it easy for partners to integrate your product or service into their customer’s journey. Examples from other industries include Stripe and PayPal for payments; Twilio, Nexmo or Wavecell (Wavecell is now 8x8) for customer communications.

Insurers’ fundamental challenge is that people don’t go looking for insurance. Insurance is a means of protecting their health, wealth or property. The journey towards discovering that need, and the potential solutions, starts elsewhere.

Adopting Open Insurance enables insurers to:

- Expand and simplify distribution

- Deepen and scale partner relationships

- Enable new business models

Expand and Simplify Distribution

Insurers have long relied on partner distribution channels. Banks, in particular, have been a strong source of new customers, as people talk to their banks when they are ready for a conversation about their financial needs. Other distribution channels include agents and brokers, and affiliates such as travel agents, real estate agents, and car dealers.

Comparison sites such as GoCompare, MoneySmart, GoBear, and iSelect aggregate information from different providers, enabling customers to find, evaluate and select the solutions that will best meet their needs.

While distributors can obtain product information in advance from providers, requesting this information in real time ensures that details are correct when the customer requests it.

Qover publishes APIs to enable partners to distribute their Home, Lifestyle and Motor insurance lines. They support two operating models:

- Lead: The focus is to generate leads out of the partner’s system to the insurer’s.

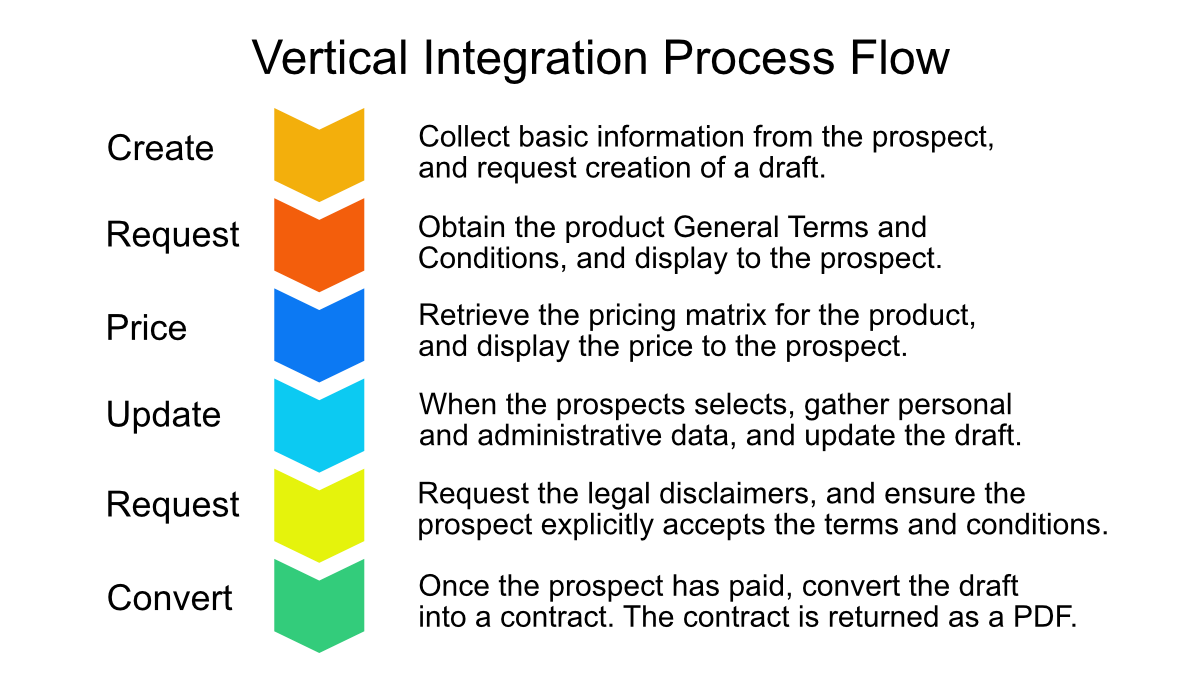

- Vertical Integration: The partner controls all communication with the customer, calling the insurer’s APIs for each step of the process flow.

The lead model is the simplest to implement, as it requires minimal coding for the partner, and uses the insurer’s existing process flows. The partner captures the minimum data necessary to create a draft, and shows details of the product to the lead. A second step sends the lead an email so that the lead can finish the flow on the insurer’s site.

Passing the lead from the partner’s system to the insurer’s, however, creates a disjointed user experience, which risks lower conversion rates from lead to prospect to customer.

Keeping the partner as the primary communicator with the prospect retains a seamless user experience. The vertical integration flow includes calls to APIs to create a draft, price it and then convert it into a contract.

AXA’s Affiliate program offers travel providers a way to increase their sales revenue while meeting their customers’ needs for travel insurance. Travel providers can choose their preferred way to partner, integrating with their website through a link, banner advertisement, widget or API.

Euler Hermes seeks to remove the risk from B2B commerce by providing insurance for trade receivables. Through APIs published under its Single Invoice Cover service, Euler Hermes enables partners such as invoice factoring firms to:

- Search the buyer and supplier

- Get a quote to protect the transaction

- Accept the quote, and activate protection

- Settle the transaction or file a claim

What do AXA, Qover, Euler Hermes, Nationwide, NTUC and AIA have in common? They are embedding insurance into the digital economy. And the building blocks they are using to do it: Application Programming Interfaces (APIs).

Partner-Managed Relationships

Nationwide Insurance of the USA has published a comprehensive set of APIs covering generating quotes and applying for policy contracts for partners such as insurance brokers and dealers, car dealerships and mortgage companies.

AXA Assistance offers a suite of APIs for partners to access and update policy holder information, submit a claim and request assistance for Roadside, Travel, Home, Health & Lifecare for customers and employees.

Connecting to multiple platforms and partners can be challenging for insurers. eBaoTech is a Platform-as-a-Service offering to connect all parties in the digital insurance ecosystem, bridging channels and business scenarios to traditional insurance core systems. InsureMO provides a full set of insurance APIs for all mainstream products and processes, including Quotation, Illustration, Proposal, Issuance, Cancellation, Endorsement, Enquiry, Claim.

New Business Models

In traditional insurance models, customers only engage with an insurance company when they sign up, when a policy comes up for renewal, or when they have a problem. In between, customers don’t think about their insurer. When they receive their renewal, a mismatch between their estimated and actual usage of a facility can lead them to question the value they receive from their policy.

New insurance models aim to engage customers throughout the life of their relationship with their insurer. These include providing customers advice in order for them to achieve better outcomes, or to tailor pricing based on customer behaviour or usage. These models are made possible by the communication between sensors monitoring the asset or person insured, and the insurer (through APIs).

AIA Vitality is a wellness program to help people get healthier by giving them the tools, knowledge, access, and incentives to improve their health. Integrating with fitness devices, the program encourages members to engage in healthy pursuits and to track their physical activity.

Nationwide’s SmartRide is a usage-based insurance program that gives drivers personalised feedback to help them make safer driving decisions. After issuing a small device that plugs into their customer’s car, they measure the customer’s driving trends and recommends improvements. At the end of the program, customers are rewarded for good driving behaviour.

In Singapore, NTUC Income’s FlexiMileage uses a telematics device installed in the customer’s car to track annual mileage travelled as a basis for setting the customer’s discounted premium.

Leveraging the APIs of Others

Insurers can also simplify processes for themselves and their customers by utilising third party services, published as APIs.

An activity common to all financial services is identity verification for the purposes of Know Your Customer (KYC) compliance. In Singapore, the government’s MyInfo service enables customers to consent to secure sharing of their personal information with the financial institution. This removes the need for customers to provide their identity documentation that the government already knows.

At a global level, Trulioo’s identity verification service lets companies instantly verify five billion individuals and 250 million business entities from anywhere in the world in real-time.

A Roadmap for Action

Insurers should see the platform economy as an opportunity to simplify their customers’ search, expand their distribution channels, and craft new solutions for their customers’ needs.

Firms should look across their customer’s entire journey, see where customers go to find solutions, and identifying discontinuities in the customer experience. Determining how best to manage the flow of information depends on the source of the information, who needs it, and how to pass it securely between the relevant parties. Finally, assess whether your own firm or your partners are best placed to address the gap.

Open Insurance, enabled by APIs, can make it easier for customers and partners to do business with you, whether as a platform, or as a plug-and-play service within a wider ecosystem.

About author

Jon Scheele helps financial services and telecommunications companies define their API strategy and roadmap, build their API team, governance and processes, and foster internal and external developer communities. Jon is the organiser of APIdays Singapore, a two-day conference on APIs, Ecosystems and Finance-as-a-Service, and a co-organiser of API Craft Singapore.