Written by Fouad Husseini, founder at The Open Insurance Initiative.

The first whitepaper of The Open Insurance Initiative, promised that a series of research papers will be published to develop the concept of an international open standard for open application interfaces (APIs) in the insurance sector. This article coincides with launch of the second whitepaper, aptly titled, “Open Insurance: a foundation for platform ecosystems”.

All signs to date indicate that we are at the nascent stages of open API adoption in the sector. The Open Insurance Innovation Lab has collected a significant amount of data on the adoption and usage of APIs by incumbents, new entrants and also companies outside the sector that provide data and services related to insurance services.

This ongoing research shows that in 2019, only 21% of incumbent insurers directly provided access to APIs, indicating that InsurTech startups are leading the way in providing accessibility to services and products. The overall picture is not a pretty one. The focus of this accessibility is on the distribution of simple insurance products with 78% of APIs doing one thing, albeit doing it very well, serve products and conclude a sale completely online. Only 10% of APIs allow for claims related functionality which clearly implies that an important element of the service still relies on offline intervention.

We expect a generalized improvement in 2020 with insurance carriers actively exploring and increasingly adopting more open platform strategies. There is so much noise though. Ecosystem orchestration has become a buzzword that generates anxiety for large and small incumbents forced to rethink business models and organizational cultures and technologies, to defend market shares threatened by big Tech platforms looking to disrupt new sectors and startups bent on dislodging well established companies.

Tech-enabled marketplaces and platforms

But the need to understand platform driven innovation is not unique to the insurance sector. We’ve already seen the rise of mega marketplaces and platform ecosystems and the resulting disruption of verticals in retail, telecommunications and travel.

Not surprisingly, tech platforms and n-sided marketplaces have become a major topic in business research. Entrepreneurs and investors alike look for cues on what factors make businesses like Google’s Android, Facebook’s communities or Airbnb’s network of hosts, outshine traditional business models and withstand the rigors of competition. There are examples a plenty of their forays into financial services that insurers view as a threat to their businesses.

Big Tech are obviously evolutionary Juggernauts with an unstoppable drive for growth and expansion. They provide obsessive customer service and a customer interface that for insurers, is hard to match with much of today’s offerings.

Their immense ecosystems were created with a powerful concoction of network effects, modularity, control points, tech and the resulting hundreds of millions of users that became locked into tools, communities and for many startups the platforms for building the next unicorn business.

Accelerating pace of change

For insurance consumers, the avant-propos is written by hundreds of startups using tech to transform every facet of the value chain. Billions of investors dollars support the development of new business models. In fact, US4.4 billion was committed in startup funding during the first 3 quarters of 2019. An ecosystem of accelerators and innovation hubs vie to attract and support cohorts of entrepreneurial teams.

Not surprisingly, many of the well-established companies in the insurance sector have sought to understand, explore and experiment in an effort to modernize and catch up with tech advancement and shifting consumer expectations.

With some foresight and anticipation, we can see that the next decade is already marked by the speed at which we are heading towards a world of hyper connectivity with data playing a bigger part in shaping the way we communicate with each other, with our homes, vehicles and with all things digital.

In Europe, open banking, by allowing easy and secure access to machine-readable customer data has become a major influence in shaping the future of banking services and has set an example for the insurance sector to follow.

There is also an interesting development going on in that some sectors, namely banking and vehicle manufacturing, where some organizations have started to realize that they can serve their own customers better. We’ve seen evidence of this at Tesla, Porsche, VW and Mercedes. Each has taken a different route to satisfy the needs of their customers, but there seems to be a trend developing driven by data analytics that these companies use to either influence the design of insurance solutions or to provide a platform and open APIs for third parties to develop new insurance products. The main focus of the trend has been on reducing the cost of insurance coverage.

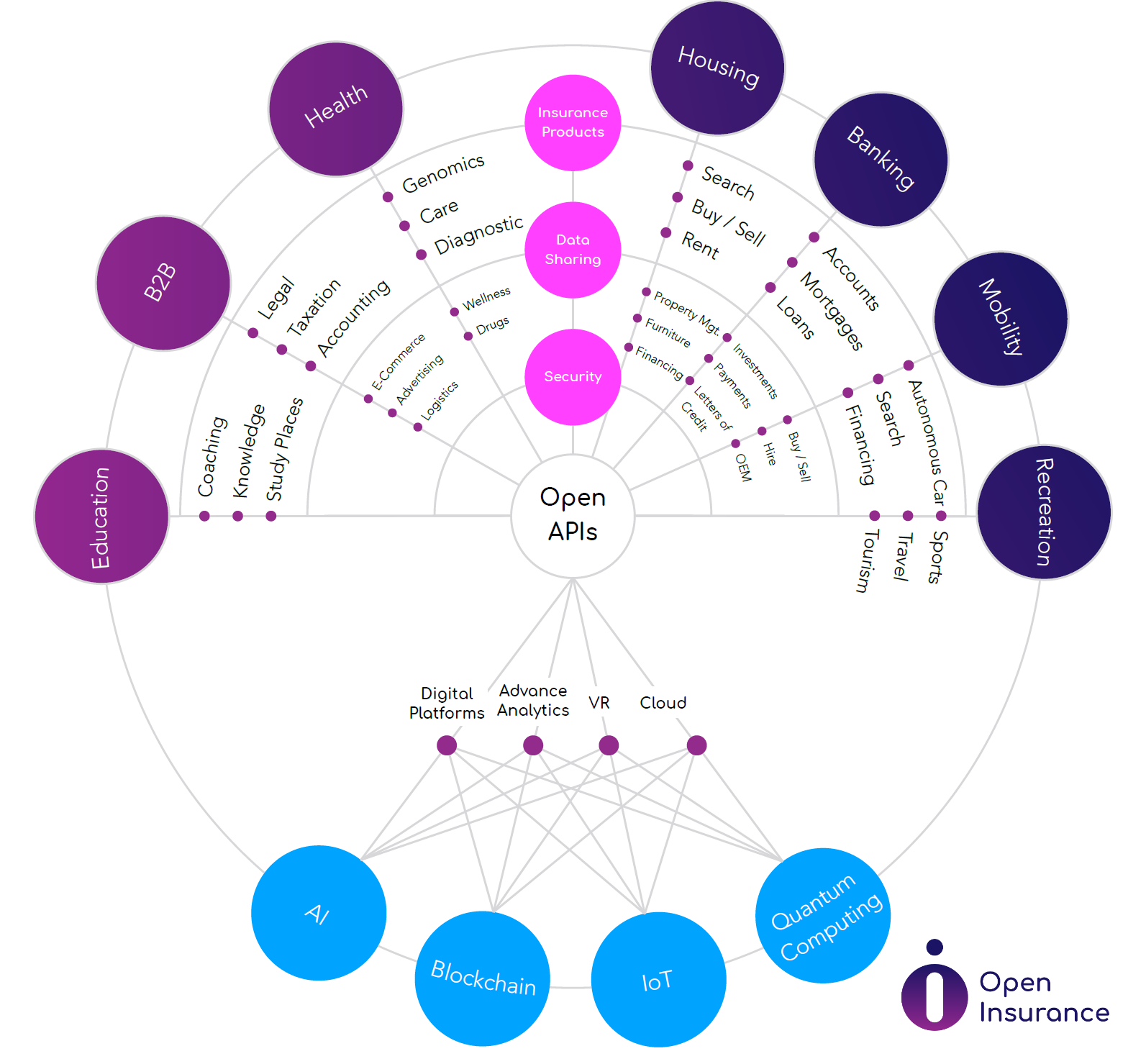

The state of insurance API market

The OPIN Innovation Lab can report that globally, the largest number of available open APIs are auto insurance related (25% of total). These provide traditional as well as usage-based insurance and roadside assistance solutions. Travel insurance and parametric flight delay insurance make up the second largest segment (20% of total). Life insurance is ranked third (17% of total open APIs), however, 95% of life APIs provide a term life insurance product. In fact, simple, individual products dominate the range of all APIs available.

Despite the ever-expanding tidal wave of InsurTech startups, the pain of point to point integration is continuing, so is the cost and time expended in receiving regulatory approvals and so has the absence of truly disruptive platforms that can build financial ecosystems of significant scale.

Since the launch of the open insurance initiative in the latter half of 2018, I have been involved in initiating literally hundreds of conversations with policymakers, regulators, incumbents, startups, technology vendors and many others across the globe.

There is always great interest in how open insurance would allow for interoperability and platforms to emerge and ecosystems to form. In my research for the second whitepaper, it was extremely hard to find serious published work that examined with a holistic approach the factors needed for insurance platform ecosystems to emerge successfully. It is undoubtedly a complex topic requiring rigorous research, experimentation and foresight.

A need to understand how platform ecosystems emerge

The second whitepaper sets out to explore a specific range of variables in a complex formula. This included defining the model features for an open insurance platform, the roles of users and complementors, factors of growth and dominance and the strains that insurance platforms need to endure as the demands of hyper-connectivity increases.

Not only that, but the basic foundations also had to be covered. For example, how is an open standard defined? What role does an open standard play in creating network effects? How do you improve data literacy of consumers and prompt them to trust open insurance in how and why their data should be shared? How do you capture external and internal open innovation logic?

Add to that the changing dynamics of business built around coalitions. For example, harnessing the demand of 5G driven hyper-connectivity that our things will require to make smart homes a reality, has forced the prima donnas of the platform world, to come together. Their aim is to co-develop an open standard to allow IoT devices of different manufacturers to communicate with each other in a realization that smart home equipment won’t reach the limits of their capability without such platform interoperability. Apple, Amazon, Google and the Zigbee alliance have come together to create the Connected Home Over IP initiative with the vision of a USB like plug-and-play protocol for the home.

In the UK, in order to enable multi-modal mobility-as-a-service, a group of companies have jointly created an open API standard to share customer data stored in different proprietary systems. This will allow data to be integrated and shared to provide a single view of a customer’s purchases and usage across multiple transport providers. The Open Transport Initiative created two API specifications. One to allow access to purchase, usage and concession data and another for transport operator information.

Travel and leisure related companies in an effort to transform to full digital ticketing and reservation created an open electronic messaging standard to ensure traveler and supplier information flow smoothly throughout the global travel, tourism and hospitality industry. The Open Travel Alliance includes a wide range of supply and service organizations including airlines, hotel, car rental, global distribution systems, solutions providers, and consultants.

These examples are extremely relevant to the insurance sector and to what the open insurance initiative is trying to introduce. The business world is increasingly converging towards open standards to allow for fast and reliable communication between different operators, systems, devices and cross sector operability. One repeating occurrence is the voluntary nature of these alliances. Another significant observation is the lower level of regulatory control and compliance that the travel, mobility and other industries enjoy. Perhaps a signal that insurance regulators need to reassess current regulatory frameworks with a view to provide better incentives for shared standards and messaging to emerge between different carriers and standards that allow for open innovation to occur at large scale.

Open Finance is around the corner

PSD2 in the European Union and Open Banking in the UK have laid the foundation for a larger financial ecosystem to develop. Most notably, The Financial Conduct Authority (FCA) in the UK, has published a Call for Input late in 2019 to explore the idea of extending Open Banking to encompass insurance, mortgages, investments and pensions to what’s called Open Finance.

The new whitepaper does not shy away from exploring ideas for platform specific supervisory oversight and the role that smarter regulation needs to play in shaping the future of cross-country platform ecosystems and international data flows.

Unfortunately, surveys to date have shown that there are roadblocks in consumer adoption of open banking with one survey indicating that only 1% of consumers have used or are using an account information service. Hardly surprising, if we consider the lack of consumer awareness of the cost savings that switching could bring them. Despite the fact that GDPR focused at giving consumers more control over access to their data, all signs so far point to that empowering consumers to share their data doesn’t really translate to more sharing of data but rather the opposite.

Consumers clearly need to trust open insurance in how and why their data should be shared if we are to avoid some of the pitfalls of open banking. That’s one of the reasons why the concept of Open Insurance Dashboards (OPIN’D) has been introduced in the second whitepaper and explained their role with use case examples. But the uptake of open insurance is not just a factor of consumer data literacy. For real uptake to happen, great apps must be developed to solve real and important problems.

That’s perhaps where an open innovation approach leveraging the external and inventive resources of customers, experts, developer communities, inventors, startups, and academics could lead to deviant solutions and killer apps.

Open insurance allows platforms, through modularity, compatibility and common standards, to become explicitly more open to external innovation. Platforms also need to provide the necessary tools for complementors -ranging from independent developers, low budget startups to heavy weight enterprises-, they have to engage with and bolster their communities. The platform age will probably unlock a larger economic pie than has ever been possible before and may usher in a new dominant financial leader.

Well established online marketplaces and platforms (the incumbents of the digital age) are constantly evaluating new opportunities to capture more transactions on their platforms and provide a unified experience leading to ownership of the whole supply experience. In many cases this will include financial components being built directly into their platforms that some are labelling as a move towards creating fintech enabled marketplaces.

Open technological interfaces in insurance will foster the Insurance-in-Everything paradigm with insurers gearing up their platform infrastructures with intelligent software components and tools to be able to interact with smart homes, autonomous vehicles, virtual courts of law and the smart cities of the future. Insurance will move closer to becoming ubiquitously embedded in everyday things.

As platform ecosystems and open interfaces advance and data is transited through thousands of connection points and applications simultaneously, we are bound to see equally inventive patterns of insurance fraud and cyber threats through data and software manipulation. Consumers must appreciate that they also have a role to play. In fact, the insurance ecosystem as a whole, must play a part in enhancing user awareness in order to change security behaviors in a meaningful way.

As the research of the OPIN Innovation Lab progresses on several levels, a third sequel is already under preparation to explore other elements involved in building open insurance interfaces. We are grateful to the more than 60 international companies that make up our community and support our research, projects and activities.